On July 4th, the one Big Beautiful Bill Act (OBBBA) was signed into law, making permanent or extending several key provisions of the 2017 Tax Cuts and Jobs Act (TCJA), while also introducing a host of new tax changes. While more detailed planning may be appropriate depending on your unique situation, Paragon’s Shaun Williams, CFA, CFP® and Ben Michalskireviewed the 870-page legislation to highlight a few provisions most likely to impact our clients:

As with any major piece of tax legislation, many provisions of the OBBBA will require clarification by the IRS. We expect additional guidance and possibly revisions to some interpretations over the coming months. We’ll keep you updated as new information becomes available.

- Current individual income tax rates made permanent:

The lower tax brackets introduced in 2018 (10%, 12%, 22%, 24%, 32%, 35%, 37%) will no longer sunset in 2026. - Standard deduction remains elevated:

The standard deduction will stay high, was raised for 2025 from $30,000 up to $31,500 for married filing jointly, and continues to be indexed for inflation. - Boosted deduction for older adults – not just about Social Security:

Individuals age 65+ with income below $75,000 ($150,000 for couples) can now claim an additional $6,000 deduction from 2025 to 2028—on top of the regular standard deduction. - The deduction phases out as a 6% effective tax until it is gone completely when income is over $175,000 ($250,000 for couples)

- This provision is often cited when the Social Security Administration states that “90% of retirees won’t pay tax on their Social Security.”

- However, this is not a change to how Social Security is taxed. It simply reduces overall taxable income, which may lower how much Social Security, or any other income, is subject to tax.

- State and local tax (SALT) deduction cap temporarily increased:

The $10,000 SALT cap rises to $40,000 in 2025 and is phased down through 2029. - The phaseout begins at $500,000 MAGI (Modified Adjusted Gross Income) and fully reverts to the $10,000 cap by $600,000.

- This phaseout effectively adds 10.5–12% in marginal tax for income within that range. We have seen some scenarios where clients could be effectively taxed over 60% for income between $500,000 and $600,000 if they live in a high-tax state like California!

- Gift & estate tax exemption increased:

Instead of falling to ~$7 million in 2026, the exemption will rise to $15 million per person, indexed for inflation starting in 2027. - Child tax credit enhanced and extended:

Increased to $2,200 per child in 2025 (up from $2,000 under TCJA and $1,000 under pre-TCJA law), with future inflation adjustments. - Pass-through business deduction made permanent:

The 20% deduction for qualified business income (QBI) is here to stay. - Mortgage interest deduction stays limited:

The deduction is permanently capped at interest on up to $750,000 of acquisition debt. - Charitable giving rules adjusted:

- For itemizers, deductions apply only to donations exceeding 0.5% of AGI.

- For non-itemizers, a new above-the-line deduction allows up to $1,000 in cash donations ($2,000 for joint filers) starting in 2026.

- Miscellaneous itemized deductions permanently repealed:

This includes things like investment advisory fees, unreimbursed employee expenses, and tax prep costs. - Qualified small business stock (QSBS) gain exclusions expanded:

Increases in excludable amounts and a new tiered structure for stock held 3–5 years.

- Available only for children born between January 1, 2025, and December 31, 2028.

- Intended to offer tax-advantaged growth, but contribution and withdrawal rules remain unclear.

- Current guidance is limited, and these accounts may be too restrictive to have a broad impact, unless a child is born during the eligible window

We’ll continue monitoring developments as more regulatory guidance becomes available.

- Higher income tax rates across most brackets

- A significantly reduced standard deduction

- A lower estate and gift tax exemption—potentially exposing more wealth to taxation

- Loss of the 20% qualified business income deduction for business owners

- Stricter limitations on deductions for state and local taxes

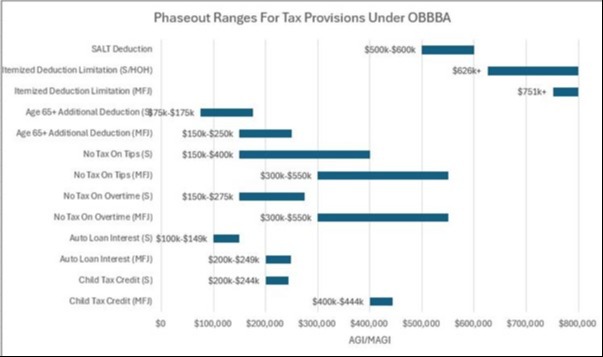

The plethora of new phaseout ranges makes for a bit of a minefield for tax planning. Being strategic and thoughtful each year can bring more value than ever before. As part of our analysis, we've mapped out where various OBBBA provisions begin to phase out across different income levels. The chart below illustrates just how critical income thresholds have become in determining who benefits most — and where strategic tax planning will matter most:

Source: Kitces.com

After a thorough evaluation of the OBBBA and its implications for our client base, we’ve identified a few trends worth highlighting:

- Timing and Magnitude of Tax Savings

The greatest savings are expected in 2026, when the TCJA would have otherwise expired. - In 2025, client tax bills are projected to decrease by 0–33%, depending on income—lower earners see the highest percentage savings.

- On average, our clients are projected to save ~6% in 2025 compared to pre-OBBBA projections.

- In 2026, projected tax savings increase to ~12%, largely due to the OBBBA’s prevention of the TCJA sunset.

- Shifts in Standard vs. Itemized Deductions

While the OBBBA permanently increases the standard deduction ($15,750 for single filers and $31,500 for joint filers in 2025), some clients who previously benefited from the standard deduction may now find it more advantageous to itemize—especially given the expanded (but phased) SALT deduction and other itemized deduction changes. A strategic review of deductions will be important to maximize tax efficiency moving forward. - Impact on High-Income Households (AGI $500,000+)

High earners will benefit most from continued lower tax brackets and higher estate tax exemptions. However, because the enhanced SALT deduction cap begins phasing out at $500,000 AGI in 2025 (and $505,000 in 2026), the immediate tax impact in 2025 may be limited. For these households, careful coordination of deductions and timing strategies will be key to realizing full benefits.

We’re here to help you navigate the complexities of this new law and identify smart strategies to reduce your tax bill. If you’d like to explore how these updates affect your financial plan, don’t hesitate to reach out. We’ll continue to update you as IRS guidance evolves.